GemForex - weekly analysis

Zusammenfassung:Consolidation for the week ahead: US inflation report to cast light on the Fed’s trajectory

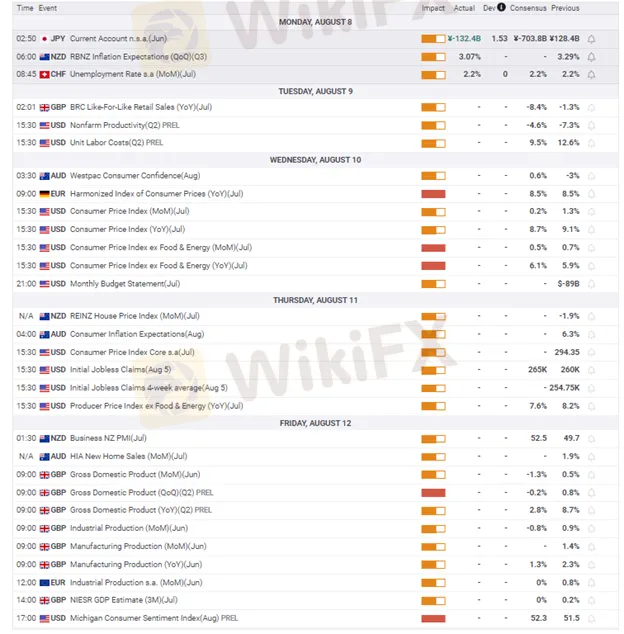

After a turbulent but interesting July and the first week of August, we are heading towards another decisive week for global markets. The main event will be the latest CPI report from the United States, which will reveal whether inflation has finally started to cool off. The economic sentiment is more mixed than expected, even after the US released stronger-than-expected employment numbers last Friday, casting doubt on the incoming recession panic.

Nevertheless, lets see what is on the shelf for the week ahead.

During the first 2 days of the week, we get employment data from Switzerland, which is expected to stay strong at 2.2%, as Switzerland reversed its dovish tune proactively before inflation worries even started and kept the Swiss economy relatively strong compared to its neighbors.

On a similar note from Europe, on Friday we get Industrial production data for the Eurozone, which after 5 months of sanctions against Russia and a significant energy shortage across major European economies, is expected to decrease ahead of the autumn season. Until Friday though, the Euro will follow and adapt to the strength of the Dollar, which if falls below the support of 1.01, could send it back to parity. A bullish breakout would put the currency back on track towards 1.290, the next important level to watch out for, something which may happen if the incoming US data will be less satisfactory than expected.

From the other side of the Atlantic, in the middle of the week, we will anticipate the CPI numbers for the US, and on Thursday the Initial Jobless claims for the month. Against the expected sentiment, the US rebounded last week due to strong employment numbers, and this week we will find out if the recessionary trend of the US economy is due to a halt or will accelerate.

On Friday, we expected the new GDP numbers from across the English Channel. Last week, the BoE measured its monetary policy and tightened the interest rate in the biggest rate hike of the last 40 years, all of that amid rapid inflation and an expected UK recession. And while inflation has already taken its toll and a looming energy crisis is around the corner, it only remains to be seen how the pound will recover, but the road ahead seems bumpy.

Despite the rate increase, the sterling suffered in the aftermath because the BoEs overall message was quite gloomy. The economic forecasts were apocalyptic, pointing to five consecutive quarters of negative GDP growth starting in the fourth quarter of this year.

WikiFX-Broker

Aktuelle Nachrichten

XRP: Was Ripple dir JETZT nicht offen sagt

WikiFX

WikiFXSolana vor möglichem Ausbruch: ETF-Zuflüsse stützen Kurs über 131 Dollar

WikiFXXRP vor Crash? Ripple-Signal warnt: minus 60% möglich

WikiFXLitecoin unter massivem Verkaufsdruck – Siebter Verlusttag in Folge

WikiFXBitMine kauft massiv Ethereum und peilt fünf Prozent des Umlaufs an

WikiFXCardano stabilisiert sich über 0,40 Dollar – Indikatoren nähren Hoffnungen auf Ausbruch

WikiFXWechselkursberechnung