US stocks end slightly lower in a choppy session after hot PPI data and mixed FOMC minutes.

Zusammenfassung:US markets mostly tread water ahead of CPI on 13th October figure, equities and the USD traded in a fairly tight range, a lack of expected chaos out of the UK and what were considered a mixed FOMC minutes saw markets in a holding pattern as traders await US inflation data.

US markets mostly tread water ahead of CPI on 13th October figure, equities and the USD traded in a fairly tight range, a lack of expected chaos out of the UK and what were considered a mixed FOMC minutes saw markets in a holding pattern as traders await US inflation data.

Though a modest drop as compared to recent times, it still marked the 6th down day in a row for the S&P 500 and Nasdaq, with the S&P 500 now down over 25% from the highs, putting it well into bear market territory.

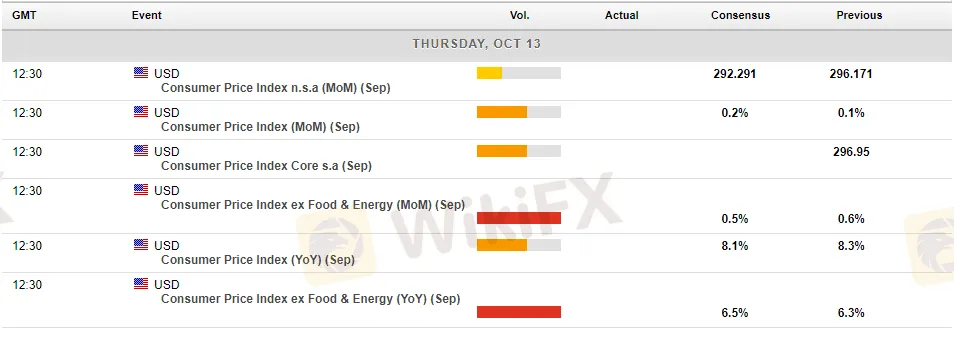

US PPI figures (Change in the price of finished goods and services sold by producers) came in at 0.4% for September, a steep rise from the previous month and handily surpassing analyst expectations of 0.2% showing that US inflation is sticking around and could bode for an elevated CPI figure later on 13th.

The VIX index (or fear index as it is sometimes known) was bid on 13th, spiking back up above 34 to touch its highest reading this month as investors rushed to hedge themselves ahead of CPI observed on 13th October.

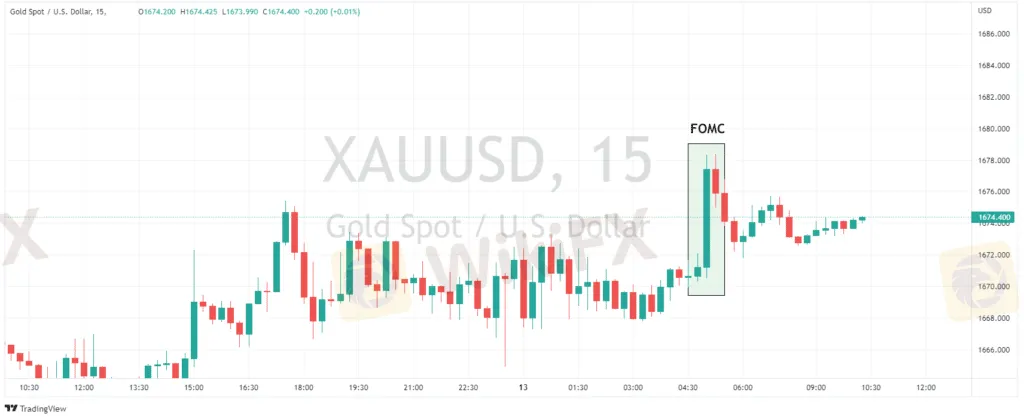

The USD had an initial rally on hot PPI figures, dipped on mixed FOMC minutes and managed to catch a bid to finish the day mostly unchanged for the day.

In commodities, Oil was down for 3rd straight day, finding support after hitting the 50% Fibonacci retracement of its October gains. This came on the back of growth concerns after a report from OPEC/EIA cutting global demand growth expectations.

Gold climbed modestly for the day, rallying after the FOMC minutes but giving that spike back late in the session as the USD caught a bid.

In economic announcements, all eyes will be on tonights US CPI figure. Analysts expects to see inflation increase 8.1% from a year ago in September. Anything above the prior reading of 8.3% should see a sharp decline in risk assets. On the flip side, a much softer reading may result in a sharp relief rally as markets re-price their Fed hiking predictions.

WikiFX-Broker

Aktuelle Nachrichten

Ozempic bald 80 Prozent günstiger? Hikma Pharmaceuticals will von auslaufenden Patenten profitieren

WikiFX

WikiFXBericht über Megaprojekt in Saudi-Arabien: Neom-Manager sollen Finanzberichte manipulieren, um hohe Kosten zu vertuschen

WikiFX„Viel zu hohe Risiken – Branchenverband für Volksbanken fordert strengere Regeln für die eigenen Banken

WikiFXFord Deutschland in den roten Zahlen – jetzt soll eine Milliarden-Finanzspritze des US-Konzerns helfen

WikiFXCorona-Überflieger Biontech machte einst Milliardengewinne – mittlerweile aber Verluste und kündigt Stellenabbau an

WikiFXIch bin 38 und CEO von Trivago: Diese 6 Skills machen euch zu einer guten Führungskraft

WikiFXWebasto: Angeschlagener Automobilzulieferer braucht 200-Millionen-Finanzspritze

WikiFXTrotz sinkendem Absatz: VW-Tochter Traton steigert Rendite und erhöht die Dividenden für Anleger

WikiFXCO₂-Ziele aufgeschoben: So soll die Autoindustrie gerettet werden

WikiFXVW-Mitarbeiter erhalten Prämie noch einmal ungekürzt

WikiFXWechselkursberechnung