Mohicans markets:MHM Today’s News

Zusammenfassung:On Thursday, October 13, the release of U.S. inflation data triggered sharp volatility across financial markets. The dollar index fell heavily below 113 after the CPI release, closing down 0.724% at 112.47. The daily volatility of the dollar index was nearly 200 points, and the yen once depreciated to the early 1990s level. The U.S. 30-year Treasury yield rose to 4%, which was the highest level since 2011. U.S. Treasury yields touched a 15-year high 2 years ago.

![第一篇[英语]](https://wzimg.ruiyin999.cn/fb_article/2022-10-14/638013536958966433/FB638013536958966433_925054.jpg-article598)

In order to further meet the needs of investors for real-time news of the international market and broaden the channels for investors to understand the market, MHMarkets launches heavily “Todays News” to provide investors with real-time market information.

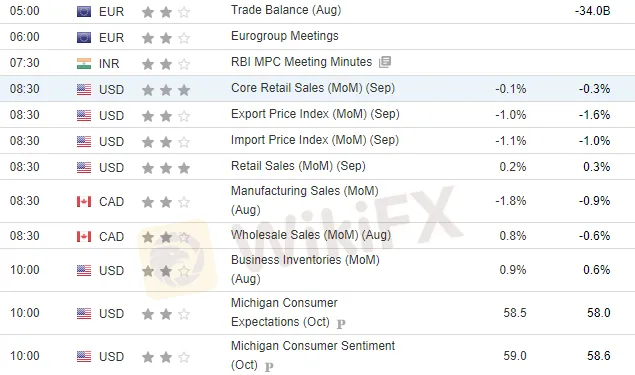

October 14, 2022--Fundamental Reminder

☆ At 09:30, China releases the annual rate of CPI for September.

☆ At 20:30, U.S. releases monthly rate of Retail Sales for September, previous value was 0.30%, and expected value was 0.20%.

☆ At 22:00, the Fed George speaks on the U.S. economic outlook; at 22:30, the Fed Governor Cook speaks on the economic outlook. Thursday‘s CPI data reignited the Fed’s aggressive rate hike expectations, and the latest statements from Fed officials are worth watching.

☆ The U.S. Treasury will hold a meeting on Friday to impose economic restrictions on Russia, with senior officials from the finance ministries and other agencies of more than 30 countries attending the meeting hosted by the U.S. Treasury.

Market Overview

——Source: jin10 & Bloomberg

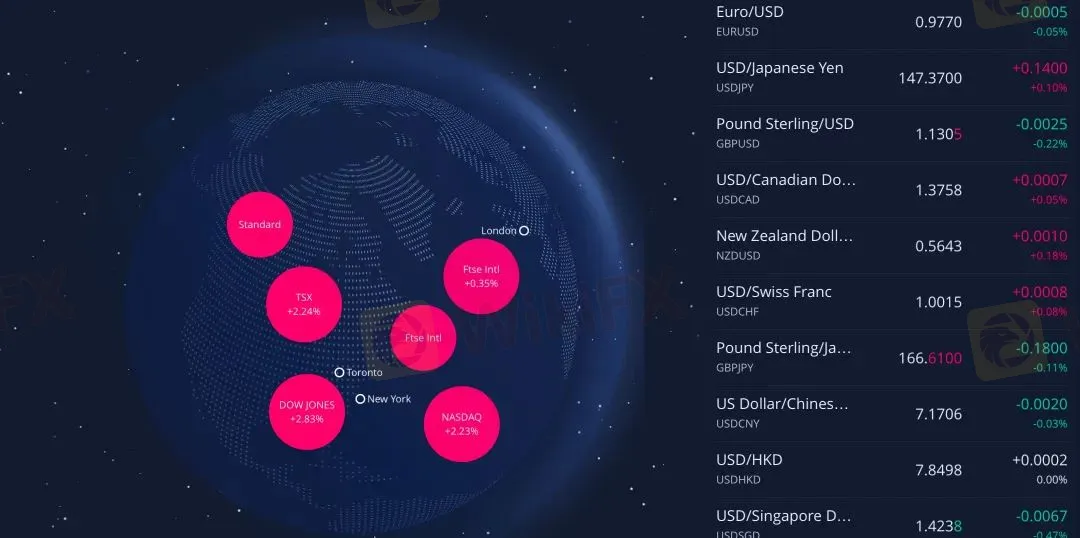

On Thursday, October 13, the release of U.S. inflation data triggered sharp volatility across financial markets. The dollar index fell heavily below 113 after the CPI release, closing down 0.724% at 112.47. The daily volatility of the dollar index was nearly 200 points, and the yen once depreciated to the early 1990s level. The U.S. 30-year Treasury yield rose to 4%, which was the highest level since 2011. U.S. Treasury yields touched a 15-year high 2 years ago. The U.S. 10-year Treasury yield once exceeded 4%.

Spot gold fell $40 from above 1680 straight to near 1642, then recovered and finally closed down 0.62% at $1,664.24 per ounce; spot silver fell below the 19 mark, closing down 0.98% at $18.88 per ounce.

Crude oil came out of an independent market, with WTI crude oil moving sharply higher in the U.S. session pushing the $90 mark, closing up 2.52% at $89.21 per barrel, while Brent crude approached $95 per barrel, closing up 2.36% at $94.55 per barrel.

U.S. stocks opened lower and closed higher, rebounding from losses triggered by high inflation data. The S&P 500 closed up 2.6%, after the index fluctuated more than 5% during the day. The Dow closed up 2.83% and the Nasdaq closed up 2.23%. Star technology stocks rose in general, Nifty rose more than 5%, Intel rose more than 4%, Nvidia, Microsoft rose about 3%, Apple rose more than 3%.

European stocks pulled up at the end of the day and closed up collectively. Germany DAX30 index closed up 1.51%; FTSE 100 index closed up 0.35%; France CAC40 index closed up 1.04%; European Stoxx 50 index closed up 0.93%; Spain‘s IBEX35 index closed up 1.16%; Italy’s FTSE MIB index closed up 1.56%.

Hot Spots in the Market

——Source: jin10&Bloomberg

1. The quarterly adjusted annual CPI rate of the United States recorded 8.2% at the end of September, the smallest increase since February 2022; The annual rate of quarterly adjusted core CPI in the United States at the end of September recorded 6.6%, the highest since August 1982; The quarterly adjusted CPI monthly rate of the United States recorded 0.4% in September, which was higher than the consensus expectation again. Data show that inflation continues to maintain a strong momentum. US short-term interest rate traders expect that the Federal Reserve's policy interest rate will reach a range of 4.75% - 5% in March 2023. The swap market is fully priced, and the Federal Reserve raised interest rates by 75 basis points in November.

2. The number of Americans who applied for unemployment benefits for the first time in the week ended October 8 recorded 228,000, a new high since September 1, 2022. US mortgage interest rates soared to a 20-year high of 6.92%.

3. Miller, president of Gazprom, said on the 13th local time that in order to repair the damaged “Nord Stream” pipeline, most of the pipeline may need to be replaced, and the repair work will continue for more than a year.

4. The EIA crude oil inventory of the United States increased by 9.88 million barrels in the week to October 7, with an expected increase of 1.75 million barrels. In that week, Cushing crude oil inventory fell for the first time in four weeks; SPR inventory decreased by 7.69 million barrels to 408.7 million barrels, a decrease of 1.85%; US domestic crude oil production decreased by 100000 barrels to 11.9 million barrels per day, the lowest level since the week of July 15, 2022.

5. EIA natural gas report: As of October 7, the total natural gas inventory in the United States was 3231 billion cubic feet, 125 billion cubic feet more than the previous week, 126 billion cubic feet less than the same period last year, a year-on-year decline of 3.8%, and 221 billion cubic feet less than the five-year average, a decline of 6.4%.

6. The British government is discussing revising the fiscal plan announced last month to prepare for reversing the tax reduction plan of Tras. They are considering which parts of the tax reduction plan may be abandoned.

7. The Saudi Foreign Ministry rarely issued a long statement defending OPEC+production cuts “completely” based on economic considerations, implying that the United States proposed to postpone production cuts until after the mid-term elections.

8. U.S. Commerce Secretary Raymond: Biden will consider some targeted tariff reductions.

9. On October 13 local time, the Special Investigation Committee of the United States House of Representatives voted to summon former President Trump to testify about the riots in the Capitol.

10. According to sources, the European Central Bank policymakers discussed the detailed timetable for reducing the 3.3 trillion euro bond portfolio earlier this month, and envisaged that quantitative tightening would begin sometime in the second quarter of 2023.

11. Russia has submitted its concerns about the Black Sea Food Export Agreement to the United Nations and is prepared to refuse to renew it next month unless its requirements are met.

12. Alcoa: The London Metal Exchange (LME) has been asked to delist Alcoa from the market, and said that the move “disproportionately” affected the aluminum contract.

13. The IEA monthly report lowered the growth forecast of global oil demand in 2022 to 1.9 million barrels per day.

14. At the beginning of next year, the European Union may file antitrust charges against Google.

Institutional Perspective

—— MHMarkets ETA

1. Brown Brothers Harriman Bank: Yellen gave the green light for the strengthening of the US dollar

2. Westpac Bank: The pound may still fall, because the support of the Bank of England is only temporary

3. Morgan Asset Management: The sharp rise of the US dollar may lead to the next crisis

4. HSBC: It is predicted that the euro will test the low point in 2022 again

5. Royal Bank of Canada: USD/JPY will rise to 150 at the end of the year

Risk warning: The margin trading of financial derivatives and other products has high risks, so it is not suitable for all investors. The loss may exceed the initial investment. Please ensure that you fully understand the risks and properly manage your risks. Any opinion, news, research product, analysis, quotation or other information in this article does not constitute the following behavior: (1) In any case, MHM will not provide investment advice or recommendation to clients, nor will it express opinions on whether clients rely on or not to make investment decisions. MHM will never provide investors with trading advice or order trading business through WeChat, QQ or other channels; (2) In any case, any materials, information or other functions provided by MHM to clients through websites, investment platforms, marketing, training activities or other means are general information, which cannot be considered as suitable for clients or suggestions based on clients' personal conditions, and MHM will not bear any responsibility for losses caused by investment based on the above information; Investors should pay attention to the official article logo of MHM and the official channel of the brand, and pay attention to identifying fake websites.

WikiFX-Broker

Wechselkursberechnung