2025-02-18 04:46

IndustryEconomic growth theories

#Firstdealoftheyearchewbacca

Keynesian Growth Theory (John Maynard Keynes)

Keynesian growth theory is more focused on the short-to-medium term and highlights the role of aggregate demand in driving economic output. In contrast to classical economics, which assumes economies tend toward equilibrium, Keynesian economics suggests that economies often operate below their potential, and government intervention can help stabilize output and employment.

Key Features:

• Aggregate Demand: According to Keynes, economic output and employment are largely determined by aggregate demand (the total demand for goods and services in the economy). If demand is insufficient, businesses cut production, leading to unemployment and unused resources.

• Government Intervention: Keynes emphasized that during economic downturns, private sector demand could collapse, and the government should step in to stimulate the economy through fiscal policies (increased government spending, tax cuts) and monetary policies (lowering interest rates). This helps maintain demand, increase output, and reduce unemployment.

• Investment and Confidence: Investment is critical to economic growth, but it is highly sensitive to confidence levels. If businesses expect future growth, they will invest in capital, which, in turn, stimulates further growth. On the other hand, pessimism can lead to a reduction in investment, exacerbating recessions.

• Short-Run Focus: Keynesian economics is primarily concerned with managing short-term economic fluctuations. Unlike classical economics, it doesn't assume that the economy naturally tends towards full employment. Rather, government intervention is seen as necessary to close output gaps.

• Multiplier Effect: One of the most important concepts in Keynesian economics is the multiplier effect. If the government increases spending, the initial increase in demand will lead to higher income and further spending, thus amplifying the initial stimulus.

Major Figure:

• John Maynard Keynes: In his seminal work The General Theory of Employment, Interest, and Money (1936), Keynes argued that economies can remain in a state of equilibrium with high unemployment for long periods if aggregate demand is insufficient. He advocated for active fiscal and monetary policies to manage the business cycle and reduce unemployment.

Implications:

• Government Policy is Key: The government plays a crucial role in mitigating economic downturns. Through spending and monetary policies, the government can help manage demand and prevent long-term stagnation.

• Counter-Cyclical Measures: In times of recession, Keynes advocated for expansionary policies to boost demand, whereas during periods of inflation, contractionary policies (reducing demand) should be implemented.

Endogenous Growth Theory (Paul Romer, Robert Lucas)

Endogenous growth theory was developed in the 1980s as a response to the limitations of classical and Keynesian models, particularly in explaining long-term, sustained growth. It shifts the focus from external factors (like technological change) to internal factors within the economy that drive innovation, knowledge, and human capital accumulation.

Key Features:

• Technological Progress is Endogenous: Unlike classical models, which treat technological progress as an exogenous factor, endogenous growth theory argues that technological innovation and progress result from intentional actions within the economy, such as investment in research and development (R&D) or human capital (education and skills).

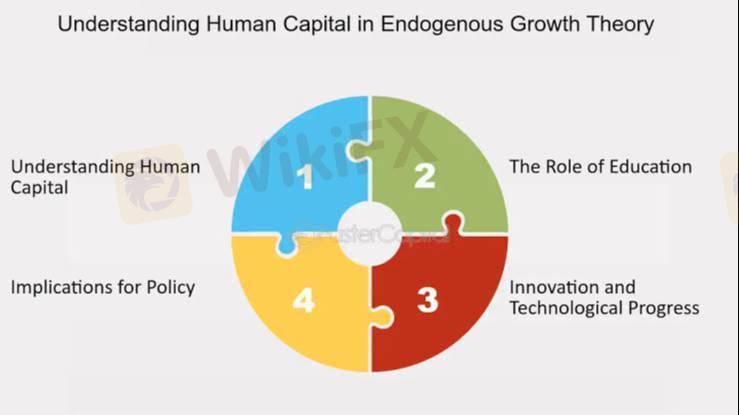

• Human Capital: Human capital plays a central role in endogenous growth. Education, training, and the accumulation of skills lead to increased productivity and innovation. More educated and skilled workers are more likely to generate new ideas and contribute to the knowledge economy.

• Knowledge Spillovers: Endogenous growth theory highlights the importance of knowledge spillovers—where ideas and innovations from one firm or industry benefit others. For example, investments in R&D by one company can lead to innovations that benefit the entire economy.

• No Diminishing Returns: In contrast to classical models, endogenous growth theory assumes that there are no diminishing returns to capital and investment. Instead, sustained investment in technology and human capital can lead to continuous and unbounded growth.

• Public Policy and Innovation: Government policies that encourage R&D, innovation, and human capital development can enhance long-term growth. For example, subsidies for R&D, patents to protect intellectual property, and investments in education can all help stimulate sustained economic expansion.

Major Figures:

• Paul Romer: Romer’s work emphasized that economic growth is driven by the intentional investment in knowledge and innovation. He introduced the concept of non-rivalrous goods (like knowledge) that, once created, can be used by many people without diminishing in value.

• Robert Lucas: Lucas focused on the role of human capital in growth, arguing that the accumulation of skills and knowledge among workers leads to higher productivity and innovation, which in turn drives growth.

Implications:

• Sustained Growth is Possible: Economic growth does not necessarily slow down over time. If countries invest in innovation, education, and knowledge, they can continue growing indefinitely.

• Role of Policy: Public policies that promote education, R&D, and innovation are crucial for long-term economic expansion. There is no inherent limit to growth as long as investment in knowledge and human capital continues.

• Capital Accumulation and Innovation: Unlike the classical model, where increasing capital leads to diminishing returns, in endogenous growth models, more investment can lead to more innovation, productivity improvements, and ultimately, sustained economic growth.

Comparison of the Three Theories:

Each theory contributes unique insights into economic growth, with the classical model emphasizing resource limitations, the Keynesian model focusing on the importance of demand and policy, and the endogenous growth model highlighting innovation and human capital as drivers of long-term prosperity.

Like 0

FX3983408141

Broker

Hot content

Industry

Event-A comment a day,Keep rewards worthy up to$27

Industry

Nigeria Event Giveaway-Win₦5000 Mobilephone Credit

Industry

Nigeria Event Giveaway-Win ₦2500 MobilePhoneCredit

Industry

South Africa Event-Come&Win 240ZAR Phone Credit

Industry

Nigeria Event-Discuss Forex&Win2500NGN PhoneCredit

Industry

[Nigeria Event]Discuss&win 2500 Naira Phone Credit

Forum category

Platform

Exhibition

Agent

Recruitment

EA

Industry

Market

Index

Economic growth theories

Hong Kong | 2025-02-18 04:46

#Firstdealoftheyearchewbacca

Keynesian Growth Theory (John Maynard Keynes)

Keynesian growth theory is more focused on the short-to-medium term and highlights the role of aggregate demand in driving economic output. In contrast to classical economics, which assumes economies tend toward equilibrium, Keynesian economics suggests that economies often operate below their potential, and government intervention can help stabilize output and employment.

Key Features:

• Aggregate Demand: According to Keynes, economic output and employment are largely determined by aggregate demand (the total demand for goods and services in the economy). If demand is insufficient, businesses cut production, leading to unemployment and unused resources.

• Government Intervention: Keynes emphasized that during economic downturns, private sector demand could collapse, and the government should step in to stimulate the economy through fiscal policies (increased government spending, tax cuts) and monetary policies (lowering interest rates). This helps maintain demand, increase output, and reduce unemployment.

• Investment and Confidence: Investment is critical to economic growth, but it is highly sensitive to confidence levels. If businesses expect future growth, they will invest in capital, which, in turn, stimulates further growth. On the other hand, pessimism can lead to a reduction in investment, exacerbating recessions.

• Short-Run Focus: Keynesian economics is primarily concerned with managing short-term economic fluctuations. Unlike classical economics, it doesn't assume that the economy naturally tends towards full employment. Rather, government intervention is seen as necessary to close output gaps.

• Multiplier Effect: One of the most important concepts in Keynesian economics is the multiplier effect. If the government increases spending, the initial increase in demand will lead to higher income and further spending, thus amplifying the initial stimulus.

Major Figure:

• John Maynard Keynes: In his seminal work The General Theory of Employment, Interest, and Money (1936), Keynes argued that economies can remain in a state of equilibrium with high unemployment for long periods if aggregate demand is insufficient. He advocated for active fiscal and monetary policies to manage the business cycle and reduce unemployment.

Implications:

• Government Policy is Key: The government plays a crucial role in mitigating economic downturns. Through spending and monetary policies, the government can help manage demand and prevent long-term stagnation.

• Counter-Cyclical Measures: In times of recession, Keynes advocated for expansionary policies to boost demand, whereas during periods of inflation, contractionary policies (reducing demand) should be implemented.

Endogenous Growth Theory (Paul Romer, Robert Lucas)

Endogenous growth theory was developed in the 1980s as a response to the limitations of classical and Keynesian models, particularly in explaining long-term, sustained growth. It shifts the focus from external factors (like technological change) to internal factors within the economy that drive innovation, knowledge, and human capital accumulation.

Key Features:

• Technological Progress is Endogenous: Unlike classical models, which treat technological progress as an exogenous factor, endogenous growth theory argues that technological innovation and progress result from intentional actions within the economy, such as investment in research and development (R&D) or human capital (education and skills).

• Human Capital: Human capital plays a central role in endogenous growth. Education, training, and the accumulation of skills lead to increased productivity and innovation. More educated and skilled workers are more likely to generate new ideas and contribute to the knowledge economy.

• Knowledge Spillovers: Endogenous growth theory highlights the importance of knowledge spillovers—where ideas and innovations from one firm or industry benefit others. For example, investments in R&D by one company can lead to innovations that benefit the entire economy.

• No Diminishing Returns: In contrast to classical models, endogenous growth theory assumes that there are no diminishing returns to capital and investment. Instead, sustained investment in technology and human capital can lead to continuous and unbounded growth.

• Public Policy and Innovation: Government policies that encourage R&D, innovation, and human capital development can enhance long-term growth. For example, subsidies for R&D, patents to protect intellectual property, and investments in education can all help stimulate sustained economic expansion.

Major Figures:

• Paul Romer: Romer’s work emphasized that economic growth is driven by the intentional investment in knowledge and innovation. He introduced the concept of non-rivalrous goods (like knowledge) that, once created, can be used by many people without diminishing in value.

• Robert Lucas: Lucas focused on the role of human capital in growth, arguing that the accumulation of skills and knowledge among workers leads to higher productivity and innovation, which in turn drives growth.

Implications:

• Sustained Growth is Possible: Economic growth does not necessarily slow down over time. If countries invest in innovation, education, and knowledge, they can continue growing indefinitely.

• Role of Policy: Public policies that promote education, R&D, and innovation are crucial for long-term economic expansion. There is no inherent limit to growth as long as investment in knowledge and human capital continues.

• Capital Accumulation and Innovation: Unlike the classical model, where increasing capital leads to diminishing returns, in endogenous growth models, more investment can lead to more innovation, productivity improvements, and ultimately, sustained economic growth.

Comparison of the Three Theories:

Each theory contributes unique insights into economic growth, with the classical model emphasizing resource limitations, the Keynesian model focusing on the importance of demand and policy, and the endogenous growth model highlighting innovation and human capital as drivers of long-term prosperity.

Like 0

I want to comment, too

Submit

0Comments

There is no comment yet. Make the first one.

Submit

There is no comment yet. Make the first one.