2025-02-17 21:38

IndustriyaHow to backtest your strategy for risk assessment

#forexrisktrip

Backtesting a strategy for risk assessment involves testing a trading or investment strategy using historical data to evaluate its performance and potential risks. Here’s a step-by-step guide:

1. Define Your Strategy: Clearly outline the rules of your strategy, including entry and exit signals, position sizing, and risk management rules.

2. Collect Historical Data: Gather relevant historical price data, including open, high, low, close, and volume. Ensure the data is accurate and covers different market conditions.

3. Choose a Backtesting Tool: Select a platform or software for backtesting, such as Python (with libraries like Backtrader or PyAlgoTrade), MetaTrader, or trading platforms like TradingView.

4. Implement the Strategy: Code your strategy into the backtesting platform. Make sure the implementation exactly follows the rules you defined.

5. Run the Backtest: Simulate the strategy using historical data, recording each trade, position size, and profit/loss.

6. Analyze Performance Metrics: Evaluate key performance indicators (KPIs) such as:

• Return on Investment (ROI)

• Sharpe Ratio (risk-adjusted return)

• Maximum Drawdown (largest peak-to-trough decline)

• Win Rate (percentage of winning trades)

• Average Win/Loss Ratio

7. Risk Assessment: Focus on metrics related to risk:

• Volatility: Measure the standard deviation of returns.

• Drawdowns: Assess frequency and severity.

• Value at Risk (VaR): Estimate potential loss under adverse conditions.

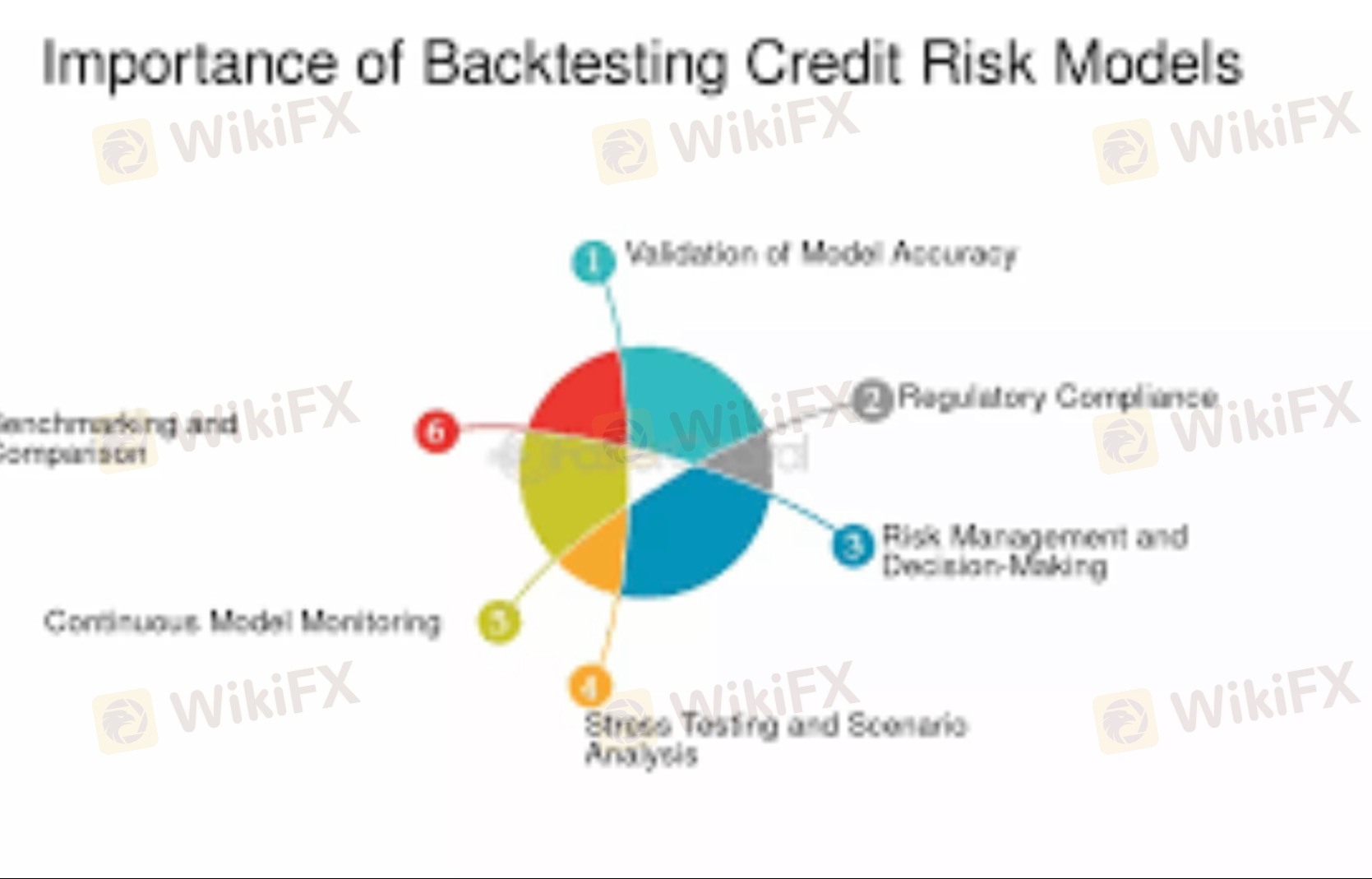

8. Validate Results: Ensure the results are statistically significant and not due to overfitting. Consider running out-of-sample tests or walk-forward analysis.

9. Optimize and Refine: Adjust strategy parameters to improve performance while avoiding overfitting. Re-test after making changes.

10. Stress Testing: Test the strategy under extreme market scenarios to see how it performs in high volatility or low liquidity conditions.

Would you like guidance on using a specific platform or coding a backtest in Python?

Katulad 0

saad940

交易者

Mainit na nilalaman

Pagsusuri ng merkado

Dogecoin cheers coinbase listing as Bitcoin’s range play continues

Pagsusuri ng merkado

Bitcoin's price is not the only number going up

Pagsusuri ng merkado

Grayscale commits to converting GBTC into Bitcoin ETF:

Pagsusuri ng merkado

Theta Price Prediction:

Pagsusuri ng merkado

How to Research Stocks:

Pagsusuri ng merkado

Bitcoin (BTC), Ethereum (ETH) Forecast:

Kategorya ng forum

Plataporma

Eksibisyon

Ahente

pangangalap

EA

Industriya

Merkado

talatuntunan

How to backtest your strategy for risk assessment

India | 2025-02-17 21:38

#forexrisktrip

Backtesting a strategy for risk assessment involves testing a trading or investment strategy using historical data to evaluate its performance and potential risks. Here’s a step-by-step guide:

1. Define Your Strategy: Clearly outline the rules of your strategy, including entry and exit signals, position sizing, and risk management rules.

2. Collect Historical Data: Gather relevant historical price data, including open, high, low, close, and volume. Ensure the data is accurate and covers different market conditions.

3. Choose a Backtesting Tool: Select a platform or software for backtesting, such as Python (with libraries like Backtrader or PyAlgoTrade), MetaTrader, or trading platforms like TradingView.

4. Implement the Strategy: Code your strategy into the backtesting platform. Make sure the implementation exactly follows the rules you defined.

5. Run the Backtest: Simulate the strategy using historical data, recording each trade, position size, and profit/loss.

6. Analyze Performance Metrics: Evaluate key performance indicators (KPIs) such as:

• Return on Investment (ROI)

• Sharpe Ratio (risk-adjusted return)

• Maximum Drawdown (largest peak-to-trough decline)

• Win Rate (percentage of winning trades)

• Average Win/Loss Ratio

7. Risk Assessment: Focus on metrics related to risk:

• Volatility: Measure the standard deviation of returns.

• Drawdowns: Assess frequency and severity.

• Value at Risk (VaR): Estimate potential loss under adverse conditions.

8. Validate Results: Ensure the results are statistically significant and not due to overfitting. Consider running out-of-sample tests or walk-forward analysis.

9. Optimize and Refine: Adjust strategy parameters to improve performance while avoiding overfitting. Re-test after making changes.

10. Stress Testing: Test the strategy under extreme market scenarios to see how it performs in high volatility or low liquidity conditions.

Would you like guidance on using a specific platform or coding a backtest in Python?

Katulad 0

Gusto kong magkomento din

Ipasa

0Mga komento

Wala pang komento. Gawin ang una.

Ipasa

Wala pang komento. Gawin ang una.