US stocks decline as weak JOLTS data and Dimon comments spook investors

Sommario:Energy shares led the way Monday as Wall Street began the week on a green note, and many overseas markets followed suit earlier Tuesday. Focus today is likely to be on the Job Openings and Labor Turnover Survey (JOLTS) data as US equities snapped a 4-day winning streak as the “bad news is good news” narrative for equities faltered in Tuesdays session.

Energy shares led the way Monday as Wall Street began the week on a green note, and many overseas markets followed suit earlier Tuesday. Focus today is likely to be on the Job Openings and Labor Turnover Survey (JOLTS) data as US equities snapped a 4-day winning streak as the “bad news is good news” narrative for equities faltered in Tuesdays session.

Job Openings and Labor Turnover Survey (JOLTS):

The latest update comes right after the market opens today. This report‘s been swollen for months, hovering close to 11 million. However, the headline number fell by 400,000 in January to 10.8 million. Analysts expect another drop, albeit to a level that’s still historically high near 10.4 million, according to Trading Economics.

Before the cash session the JOLTS job openings figure was released and came in much lower than expected, this is a key gauge of US labour market tightness that the Fed has referenced throughout its aggressive interest rate hiking cycle, and was closely watched, especially ahead Fridays NFP figure.

Rate hike odds for May dropped to 40%, this was not enough to rescue equities though as recession fears took over , the Dow , Nasdaq and S&P 500 all finishing down around 0.5%

Equity markets werent helped either by comments from Jamie Dimon of JP Morgan in his annual letter to shareholders where he stated that the banking crisis “is not over yet” and would have “repercussions for years to come.” This saw small and mid size banking stocks take a big hit, dragging down the Russell 2000 by almost 2%

In Forex the repricing lower of rate expectations saw the USD lower in the session, with the US dollar index take a 101-handle hitting its lowest level since February and sitting on a critical support level.

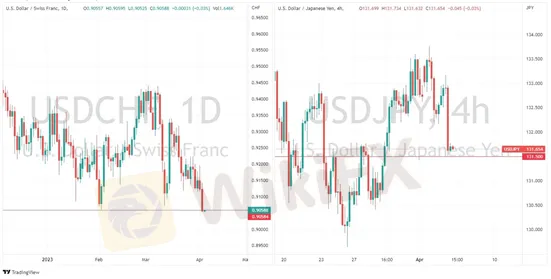

Safe havens currencies the CHF and JPY, both outperformed the greenback on risk-off conditions

USD/CHF hovering around 0.9050, the bottom of the days range and another major support level, while USD/JPY hit a low of 131.53 as the Yen ran out of momentum just above the psychological 131.50 level.

The Aussie dollar was the clear laggard in wake of the RBA rate decision, where it held rates after 10 straight hikes. This saw the AUDNZD giving up all of Mondays gains and trading under 1.07 level, just above major support at 1.0670.

In commodities, Oil managed to hold its gains from Yesterdays gap up with the surprise voluntary cut by OPEC over the weekend continuing to underpin prices.

Gold was a big mover as a weaker dollar, lower rates and risk-off saw it smash through the top of it‘s recent trading range, hitting it’s highest level in 12 months, settling around the 2020 USD an ounce level.

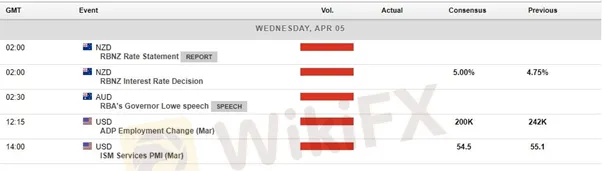

In todays economic announcements, more employment data from the US which again will be closely watched ahead of Fridays NFP, at the same time Canadian employment figures will be released, USDCAD traders beware. We also have a rate announcement from the RBNZ where a 25bp hike is expected and priced into the markets.

WikiFX Trader

FXTM

XM

FXCM

AVATRADE

Ultima

EC markets

FXTM

XM

FXCM

AVATRADE

Ultima

EC markets

WikiFX Trader

FXTM

XM

FXCM

AVATRADE

Ultima

EC markets

FXTM

XM

FXCM

AVATRADE

Ultima

EC markets

Rate Calc