Gold and Silver Rebound on Weak NFP Numbers. Crude Brent falls to $70 a barrel.

Sommario:Key TakeawaysU.S. stocks extended their record-breaking rally, with the Dow Jones surpassing 53,000 for the first time.Gold and silver surged after a weaker-than-expected U.S. jobs report, as June Non

Key Takeaways

U.S. stocks extended their record-breaking rally, with the Dow Jones surpassing 53,000 for the first time.

Gold and silver surged after a weaker-than-expected U.S. jobs report, as June Non-Farm Payrolls came in at just 57,000.

Oil prices remained under pressure, falling to around $70.20 per barrel during the week before recovering slightly.

USDJPY climbed to levels not seen in four decades, reflecting the widening policy divergence between the Federal Reserve and the Bank of Japan.

Investor sentiment remained broadly positive, driven by resilient corporate earnings expectations, and continued strength in the U.S. economy.

U.S. Equity Markets Extend Record-Breaking Rally

U.S. equities delivered another impressive week of gains, with all three major indices finishing higher and both the Dow Jones and the S&P 500 reaching fresh all-time highs. Investor sentiment remained supported by resilient corporate earnings expectations, easing concerns over an imminent Federal Reserve rate hike following weaker-than-expected employment data, and continued optimism surrounding the U.S. economic outlook.

The Dow Jones Industrial Average led the market once again, opening the week at 51,800 before climbing to a record high of 53,063. The index closed the week around 52,926, posting a gain of approximately 2.17%. The continued outperformance of the Dow reflects strong buying interest in industrial, financial, and value-oriented stocks, which have benefited from improving economic sentiment and expectations of stable monetary policy.

The S&P 500 also continued its record-breaking run. After opening the week at 7,341, the benchmark index rallied to an all-time high of 7,541 before ending the week around 7,499. This represents a weekly gain of roughly 2.15%, highlighting the broad-based strength across multiple sectors, including financials, industrials, healthcare, and technology.

Meanwhile, the Nasdaq 100 maintained its upward momentum despite some profit-taking toward the end of the week. The technology-heavy index opened at 29,021, surged to a new record high of 30,325. Although semiconductor and AI-related stocks experienced some volatility, continued investor enthusiasm for artificial intelligence and large-cap technology companies helped keep the Nasdaq near historic highs.

Oil Suffers Another Weekly Decline

Oil prices remained under pressure for most of the week, with brent crude falling toward $70.20 per barrel before recovering modestly into the weekend.

The decline reflected improving confidence that the recent U.S.–Iran peace agreement will keep supply disruptions limited, together with easing geopolitical risk premiums that had previously supported energy prices. In addition, investors remained concerned that slower global economic growth could soften fuel demand during the second half of the year.

Although prices bounced from weekly lows, oil continues trading well below the highs reached during the Middle East conflict in June.

USDJPY Continues Historic Rally

USDJPY extended its long-term uptrend and continued trading at levels not seen in approximately 40 years, highlighting the widening monetary policy divergence between the Federal Reserve and the Bank of Japan.

The pair experienced increased volatility during the week after traders suspected another round of unofficial intervention by Japanese authorities. Sharp intraday declines were followed by rapid recoveries, a pattern that has become increasingly common whenever the exchange rate approaches new multi-decade highs. Despite these interventions, the broader trend remains bullish as long as U.S. interest rates stay significantly above Japanese rates.

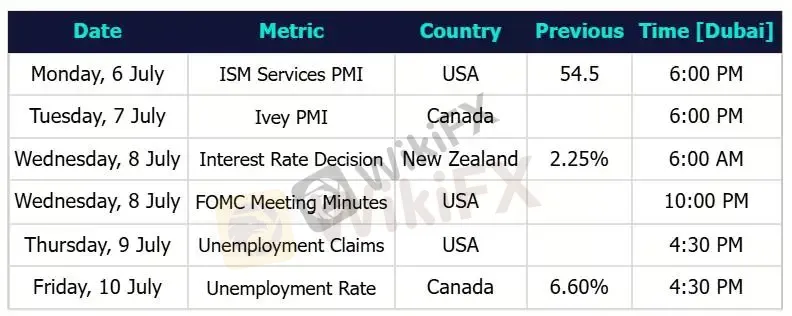

Outlook for the Week Ahead (6 – 10 July 2026)

Markets are expected to remain focused on whether the softer employment report represents the beginning of a broader slowdown in the U.S. economy or merely temporary weakness.

The release of the Federal Open Market Committee meeting minutes will likely be the week‘s most important event. Investors will look for additional insight into policymakers’ discussions surrounding inflation risks and the possibility of future rate hikes after Junes hawkish hold.

Any indication that officials remain concerned about persistent inflation could support the U.S. dollar while limiting gains in gold and equities.

Additionally, gold‘s ability to hold Thursday’s breakout will be closely monitored. Continued weakness in economic data or a more dovish interpretation of the Fed minutes could allow the metal to extend its recovery.

Conversely, if Fed officials sound more hawkish than markets expect, some of this weeks gains could be retraced.

Oil traders will continue monitoring developments surrounding Middle East supply, OPEC+ production expectations, and global demand forecasts. While prices have stabilized near $70, further downside cannot be ruled out if demand concerns continue to outweigh geopolitical risks.

Major Economic Calendar Events for the Upcoming Week

WikiFX Trader

WikiFX Trader

Rate Calc