Mohicans markets:October 27--MHM Today’s News

Sommario:On Wednesday, October 26, the dollar index fell below the 110 mark for the first time since Sept. 20, closing down 1.073% at 109.7. Non-U.S. currencies rebounded sharply, with the euro regaining parity against the dollar for the first time since Sept. 20.

![第一篇[英语]](https://wzimg.ruiyin999.cn/fb_article/2022-10-27/638024777183494616/FB638024777183494616_994057.jpg-article598)

October 27, 2022 - Fundamentals Reminder

☆ 20:15 The ECB announces its interest rate resolution. The ECB is expected to start the negotiation process of reducing its balance sheet. This shift will mark the ECBs increased efforts to remove monetary stimulus in a bid to reduce inflation. Experts warn that the ECB opens quantitative tightening may cause market turmoil.

☆ 20:45 ECB President Lagarde holds a press conference.

☆ 22:30 U.S. EIA natural gas storage for the week ending Oct. 21.

Global Market Trends Review

On Wednesday, October 26, the dollar index fell below the 110 mark for the first time since Sept. 20, closing down 1.073% at 109.7. Non-U.S. currencies rebounded sharply, with the euro regaining parity against the dollar for the first time since Sept. 20; the offshore yuan rose above 7.19 against the dollar during the day, up nearly 1,600 points from the intra-day low, as the market expects the economic slowdown to cause the Federal Reserve to ease monetary tightening after next week's interest rate After the decision to ease monetary tightening policy. The inverse of the Fed's favored 3-month and 10-year U.S. bond yields indicates that a U.S. recession may be close at hand.

Spot gold rose above 1674, pulling up more than $37 from the daily low, and finally closed up 0.72% at $1664.79 per ounce; spot silver closed up 1.61% at $19.64 per ounce.

Crude oil surged higher, defying a big increase in U.S. inventories; WTI crude rose above $89 per barrel, closing up 3.87% at $89.04 per barrel; Brent crude stood at $96 per barrel, closing up 2.94% at $96.41 per barrel.

U.S. stocks opened lower and were brought down by tech giants; although the Dow and S&P turned up mid-day, the Nasdaq was dragged down by tech earnings and failed to reverse the decline. As of the close, the Dow was close to a flat close, the Nasdaq and S&P 500 closed down 2.04% and 0.74% respectively, ending a three-game winning streak.

European stocks generally closed up, Germany's DAX30 index closed up 1.09%, the FTSE 100 index closed up 0.61%, France's CAC40 index closed up 0.41%, the European Stoxx 50 index closed up 0.55%, Spain's IBEX35 index closed up 0.99%,and Italy's FTSE MIB index closed up 0.45%.

Market Focus

——Source: jin10 & Bloomberg

1. Foreign media reported that the Biden administration considered reworking the Russian oil price cap plan at a higher price than previously expected.

2. U.S. 30-year fixed mortgage exceeds 7% for the first time in 20 years.

3. According to Reuters cited sources: Tesla faces a criminal investigation by the U.S. Department of Justice into its assisted driving system AutoPilot.

4. U.S. National Security Council spokesman Kirby: the United States does not seek a new round of negotiations on the Iran nuclear deal. The differences with Iran are too great for meaningful negotiations to take place at this time.

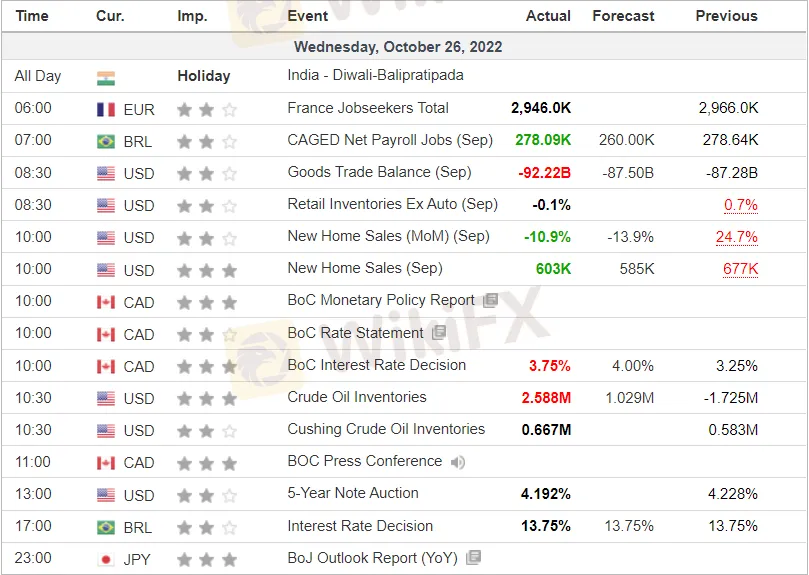

5. The Bank of Canada raises interest rates by 50BP, below market expectations of 75BP, with the highest level of interest rates since January 2008. The Bank's Governor McCollum said that the tightening phase will be nearing its end.

6. Bank of Canada: Canada may experience a technical recession between Q4 in 2022 to the end of Q2 in 2023.

7. The dollar index DXY fell below 110 for the first time in a month. U.S. crude oil exports hit a record high through the week of Oct. 21. Former U.S. Treasury Secretary Steven Nutsin expects the U.S. 10-year Treasury yield to peak at 4.5%.

8. Integrated British media reported that the U.K.'s medium-term fiscal plan was postponed to Nov. 17 for announcement; Sunac is considering tax increase.

9. WB: Russia's oil exports could fall by as much as 2 million b/d due to EU embargoes, insurance and shipping restrictions; energy prices are expected to fall 11% by 2023 after rising 60% in 2022.

(Jinshi Data APP)

Geopolitical Situation

Conflict Situation:

1. A spokesman for the emergency services of the Kherson region said on 26th that Ukrainian troops shelled the city of Novokahovka there overnight and that air defense systems shot down four Hymas rockets.

2. According to the Washington Post, Ukrainian troops continued to advance into Russian-held areas in the southern Kherson region on Tuesday and pushed back Russian mercenaries in Bakhmut in the Donetsk region.

3. According to Interfax, Putin said he was aware of Ukraine's plans to use dirty bombs.

4. According to media reports, Russian President Vladimir Putin inspected nuclear force exercises.

5. Ukraine's defense minister: personally, he doesn't think Putin will use nuclear weapons.

Food Situation:

1. European diplomats: Putin may use the extension of the UN-brokered Black Sea food deal as leverage at the G20 summit, which could eventually allow the Black Sea food deal to be rolled over or extended for a longer period of time.

2. UN aid commissioner: “relatively optimistic” that Ukraine's Black Sea food export deal will be extended.

Energy Crisis:

1. Turkey's Energy and Natural Resources Minister said Russia and Turkey reached a basic agreement to build a gas hub and Turkey has started work on its own part.

2. Saudi Aramco CEO: Oil market is realigning because of Russian discounts; there is still a lot of uncertainty in the market until the West implements measures to cap Russian oil prices.

3. Ukraine's electricity company announced that the country All categories of customers will be restricted from October 26.

4. Saudi Energy Minister: Saudi crude oil supplies to Europe doubled year-on-year in September.

5. Gas Exporters Forum says supply constraints may last until 2025 as escalating conflict triggers global energy crisis.

6. World Bank: Russia's oil exports could fall by as much as 2 million b/d due to the EU embargo, insurance and shipping restrictions.

7. Macron will unveil new corporate energy aid on Friday.

(News source: Jinshi Data)

Institutional Perspective

1. Goldman Sachs:Goldman Sachs Group strategists said conditions for a bottom in U.S. stocks are not yet visible, as they do not fully reflect the recent rise in real yields and the rising likelihood of a recession.

2. SOCIETE GENERALE:GBP implied volatility declines, but recovery appears limited.

3. MUFG:If the Bank of Canada raises rates by only 50 basis points, the USDCAD will only rebound slightly.

Statement | Disclaimer

Disclaimer: The information contained in this material is for general consultation only. It does not take into account your investment objectives, financial situation or special needs. We have made every effort to ensure the accuracy of the information as of the date of publication. MHMarkets makes no warranty or representation on this material. The examples in this material are for illustrative purposes only. To the extent permitted by law, MHMarkets and its employees shall not be liable for any loss or damage arising from any information provided or omitted in this material in any way (including negligence). The characteristics of MHMarkets' products, including applicable fees and charges, are outlined in the product disclosure statement provided on MHMarkets' website. Derivatives may be risky; The loss may exceed your initial payment. MHMarkets recommends that you seek independent advice.

MohicansMarkets, (abbreviation: MHMarkets or MHM, Chinese name: Maihui), Australian Financial Services License No. 001296777.

WikiFX Trader

Tickmill

SBCFX

Exness

FOREX.com

eightcap

VT Markets

Tickmill

SBCFX

Exness

FOREX.com

eightcap

VT Markets

WikiFX Trader

Tickmill

SBCFX

Exness

FOREX.com

eightcap

VT Markets

Tickmill

SBCFX

Exness

FOREX.com

eightcap

VT Markets

Rate Calc