Mohicans markets:MHM Today News

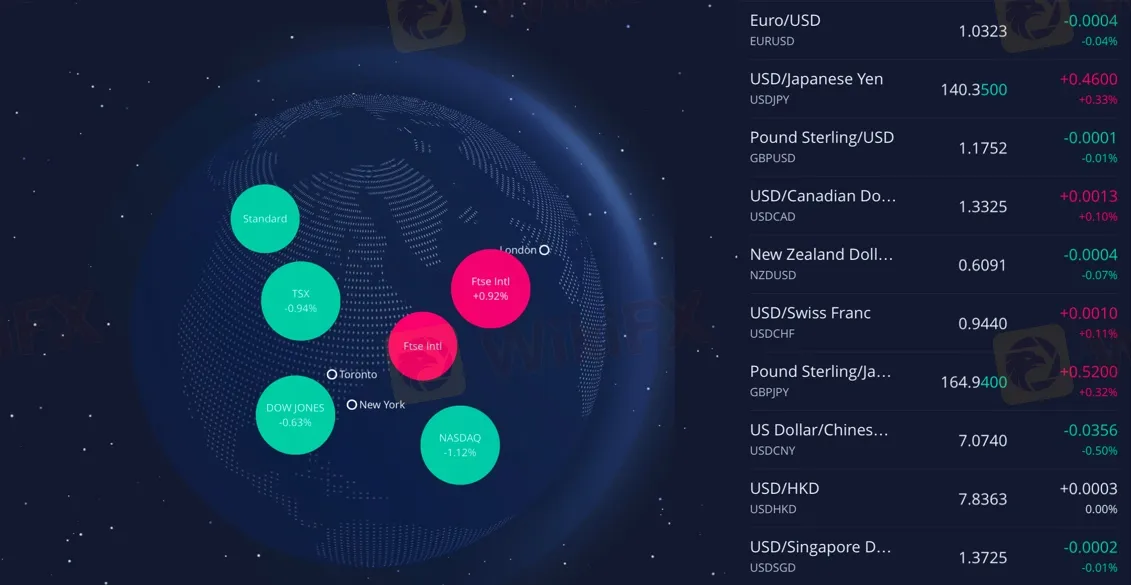

Abstract:On Monday (November 14), the US dollar index rebounded above 107, but after Fed officials said they might soon slow down the pace of interest rate hikes, the US dollar index's rise narrowed, and finally ended up 0.44% at 106.88.

![第一篇[英语]](https://wzimg.ruiyin999.cn/fb_article/2022-11-15/638041251067376196/FB638041251067376196_905195.jpg-article598)

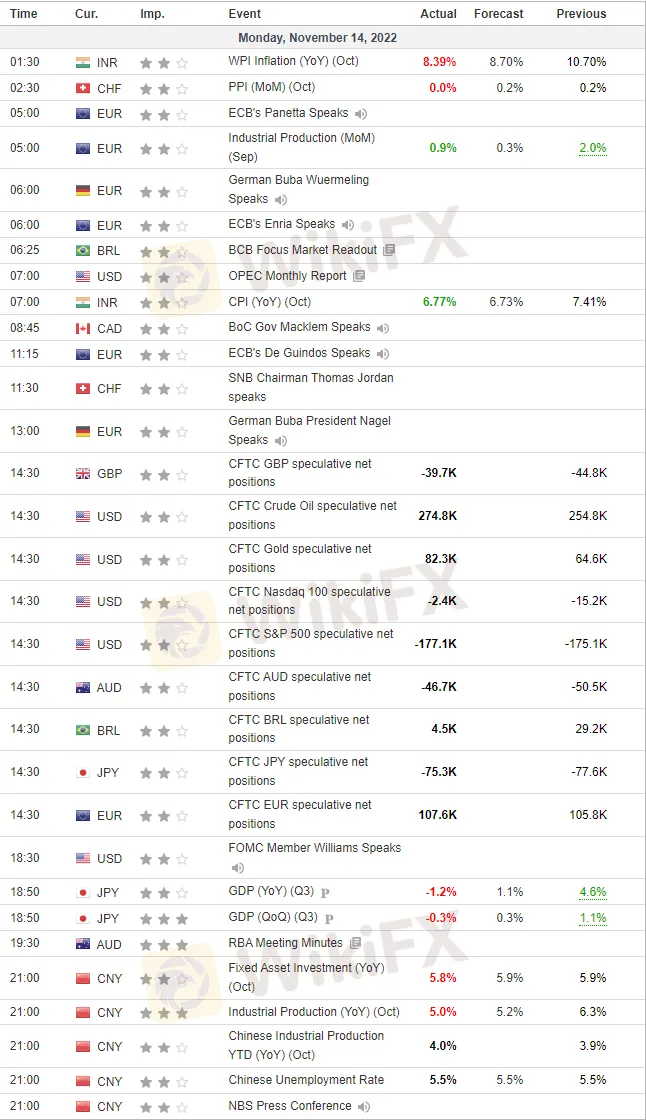

November 15, 2022 - Fundamentals Reminder

☆ The G20 Summit is to be held.

☆ At 17:00, IEA released the monthly crude oil market report.

☆ At 18:00, the euro area announced the revised annual GDP rate in the third quarter, and the ZEW economic climate index of the euro area and Germany in November. Investors will learn more about the ECB's dovish turn and the risk of a euro zone recession.

☆ At 21:30, the US announced the monthly PPI rate in October and the manufacturing index of the New York Federal Reserve in November.

☆ 22:00 Federal Reserve Hack delivers a speech on economic prospects.

Market overview

Review of global market trend

On Monday (November 14), the US dollar index rebounded above 107, but after Fed officials said they might soon slow down the pace of interest rate hikes, the US dollar index's rise narrowed, and finally ended up 0.44% at 106.88.

The yield of US bonds rose again collectively, and the yield of short-term bonds rose even more. The yield of two-year US bonds broke 4.44% in the session and fell back to 4.39% in the closing; The yield of 10-year US Treasuries fell to 3.86% after breaking 3.90% in the session. The CFTC report shows that speculators' short bets on US two-year treasury bond futures have reached the highest level since at least 1990.

Spot gold fluctuated sharply, falling 1% at one time and reaching a daily low of around US $1753. Later, with the decline of the US dollar, the gold price rebounded, and finally managed to close 0.01% higher at US $1771.49 per ounce; Spot silver broke through $22/oz in the session, closing 1.27% higher at $21.98/oz.

Crude oil fell ahead of the US market due to the strong US dollar and worrying demand outlook. WTI crude oil fell 4.17% to 85.21 dollars/barrel; Brent crude oil closed 3.49% lower at USD 92.48/barrel.

After opening low, the US stock market turned higher, and then accelerated its decline again in the late afternoon. The three major stock indexes collectively closed down, with the Dow closing down 0.63%, the Nasdaq and the S&P 500 closing down about 1.12% and 0.85% respectively.

European stocks generally gained, with Germany's DAX30 index up 0.62%, Britain's FTSE 100 index up 1.04%, France's CAC40 index up 0.22%, Europe's Stoxx 50 index up 0.5%, Spain's IBEX35 index up 0.85%, and Italy's FTSE MIB index up 0.59%.

Market Focus

1. Freeport, a major U.S. LNG exporter, said its LNG terminal may not restart until December.

2. Warren Buffett took a $4.1 billion position in TSMC in the third quarter, holding $11.9 billion worth of Occidental Petroleum stock.

3. Reports of an explosion at a small nickel pig iron plant in Indonesia triggered a 15% halt in LME nickel yesterday.

4. British Prime Minister Sunac plans to raise the minimum wage.

5. CFTC: Speculators' short bets on U.S. 2-year Treasury futures reached the highest level since at least 1990.

6. New York Fed: U.S. inflation is expected to be 5.9% one year from now.

7. OPEC cut its full-year 2023 world oil demand growth forecast to 2.24 million barrels per day.

8. FED Vice Chairman Brainard said on the FTX incident that the crypto industry is proving to be highly centralized and interconnected, not decentralized; CFTC Chairman: This cryptocurrency crisis is enough to push the U.S. Congress to act.

Geopolitical Situation

Assistance Situation:

1. Swiss President: Despite pressure, Switzerland will not provide weapons to Ukraine.

2. Ukraine's cabinet says the Netherlands will provide a loan of up to 200 million euros.

3. Ukrainian Finance Minister: Ukraine is expected to receive $4.8 billion in external aid in November and $3 billion in external financing is expected in December.

4. Canada will provide another C$500 million in military aid to Ukraine.

Energy Situation:

1. The Polish government's forced takeover of Gazprom's stake in Europopol Gas.

2. Germany's average gas storage level is close to 100%, and German regulators say some storage reservoirs can be filled further even after reaching 100% of capacity.

3. Hungary decided to set up an independent energy sector to cope with the energy crisis.

4. The German government decided to nationalize the former Gazprom subsidiary SEFE due to its excessive debt and threat of bankruptcy.

Sanction Situation:

1. The United States will impose sanctions on 14 individuals, 28 entities and 8 aircraft, including Russian billionaire Suleiman Abusadovich Kerimov.

2. European Commission President von der Leyen: The oil price cap is expected to be implemented by the end of this year and the EU is basically ready to implement the plan.

Institutional Perspective

1. Goldman Sachs:German swap spreads are expected to tighten further.

2. SOCIETE GENERALE:Shorting GBPJPY may be a more attractive trading strategy.

3. MUFG:A potential split in the U.S. Congress could hit the dollar.

Statement | Disclaimer

Disclaimer: The information contained in this material is for general consultation only. It does not take into account your investment objectives, financial situation or special needs. We have made every effort to ensure the accuracy of the information as of the date of publication. MHMarkets makes no warranty or representation on this material. The examples in this material are for illustrative purposes only. To the extent permitted by law, MHMarkets and its employees shall not be liable for any loss or damage arising from any information provided or omitted in this material in any way (including negligence). The characteristics of MHMarkets' products, including applicable fees and charges, are outlined in the product disclosure statement provided on MHMarkets' website. Derivatives may be risky; The loss may exceed your initial payment. MHMarkets recommends that you seek independent advice.

MohicansMarkets, (abbreviation: MHMarkets or MHM, Chinese name: Maihui), Australian Financial Services License No. 001296777.

Read more

Mohicans markets:MHM European Market

Spot gold weakened slightly during the Asian session on Thursday (April 6), hitting a two-day low of $2007.89 per ounce and now trading near $2014.15. A series of weak economic data has fueled fears of an impending recession in the US, giving safe-haven support to the dollar. And some dollar shorts took profits, and gold bulls also took profits ahead of Good Friday and the non-farm payrolls data, putting pressure on gold prices.

Mohicans markets:MHM Today News

On Wednesday, as the less-than-expected March "ADP" data and non-manufacturing PMI data fueled market concerns about an economic slowdown and spurred bets that the Federal Reserve could slow interest rate hikes. Spot gold continued to brush a new high since March last year, which was the highest intraday to $2032.13 per ounce, and then retracted most of the day's gains, finally closing up 0.01% at $2020.82 per ounce; spot silver hovered around $25 during the day, finally closing down 0.21% at $2

Mohicans markets:MHM European Market

Spot gold oscillated slightly lower during the Asian session on Tuesday (April 4) and is currently trading around $1980.13 per ounce. The dollar index rebounded mildly after a big drop overnight, putting pressure on gold prices. However, this week will see the non-farm payrolls report, there is no important economic data out on Tuesday, and the market wait-and-see sentiment is getting stronger.

Mohicans markets :MHM Today News

On Monday, in OPEC + members unexpectedly cut production reignited market concerns about long-term inflation and sparked uncertainty about the Fed's response, the dollar index once up to the 103 mark, and then on a "vertical roller coaster", giving back all the gains of the day and once lost 102 mark, finally closed down 0.53% at 102.04; U.S. 10-year Treasury yields rose and then fell, as data showed that the U.S. economy continues to slow, it fell sharply in the U.S. session, and once to a low

WikiFX Broker

Latest News

StoneX Review 2026: Should You Trade with This Broker?

WikiFX

WikiFXYen Firms While Dollar Pauses

WikiFXGFS Review 2026: Withdrawal Complaints, Weak Regulation Data, and Account Access Risks

WikiFXTRANS X MARKETS Review 2026: Unregulated Status and Serious Withdrawal Complaints

WikiFXRyvoTrade Review 2026: Unregulated Status and Withdrawal Complaints

WikiFXPhillip Nova Review 2026: Should You Trade with This Broker?

WikiFXThinking About KATOPRIME? What Every Trader Should Know Before Depositing Funds

WikiFXYour Backtesting Results Mean Nothing If You Ignore This One Live Trading Reality

WikiFXOver US$2.9 Million Saved: Singapore's Crypto Scam Crackdown Sends a Warning to Malaysian Investors

WikiFXHow Pig Butchering Scams Drain Beginner Trading Accounts

WikiFXRate Calc