Oil Jumps on US-Iran Tensions as Supply Fears Return; Stocks Hold Resilient

Abstract:Key TakeawaysU.S. equities lost momentum as rising oil prices and geopolitical uncertainty outweighed positive corporate earnings.The FOMC minutes reinforced a cautious Federal Reserve, showing policy

Key Takeaways

U.S. equities lost momentum as rising oil prices and geopolitical uncertainty outweighed positive corporate earnings.

The FOMC minutes reinforced a cautious Federal Reserve, showing policymakers remain divided on interest rates.

The U.S. dollar weakened overall, as softer labor market expectations offset the Feds relatively hawkish stance.

Oil prices surged on supply disruption fears, reviving inflation concerns and reducing expectations that the Federal Reserve will ease monetary policy anytime soon.

Gold remained resilient despite volatility, recovering above $4,100 as the weaker U.S. dollar provided support.

U.S. Stock Market

U.S. equities finished the week on a cautious note. The Dow Jones, S&P 500, and Nasdaq all faced pressure as rising oil prices revived inflation concerns and reduced expectations for near-term Federal Reserve rate cuts. Although technology stocks found intermittent support from semiconductor shares, overall market sentiment weakened as geopolitical risks intensified.

Economic data also painted a mixed picture. The ISM Services PMI remained in expansionary territory, indicating that the U.S. services sector continues to grow. However, the report did little to change investors‘ outlook, as markets remained far more focused on inflation risks and the Federal Reserve’s next policy move.

The release of the FOMC Minutes was one of the weeks most closely watched events. The minutes revealed that policymakers remain divided on the future path of interest rates. While some members believe rates may eventually move lower, officials also expressed continued concern that inflation remains above target and acknowledged that further policy tightening could still be necessary if price pressures persist. Overall, the minutes reinforced the view that the Federal Reserve is likely to remain data-dependent and cautious rather than rushing into policy easing.

Forex Market

The U.S. dollar weakened against most major currencies during the week despite persistent geopolitical uncertainty. The primary driver behind the softer dollar was growing market expectations that the Federal Reserve may delay additional rate hikes following weaker U.S. employment data released at the end of the previous week. Although the FOMC minutes maintained a relatively hawkish tone, they failed to provide a strong catalyst for renewed dollar buying.

The New Zealand dollar outperformed after the Reserve Bank of New Zealand raised its official cash rate by 25 basis points to 2.50%, signaling confidence in the countrys economic recovery while remaining focused on inflation.

Meanwhile, the Japanese yen received support after Japans Finance Minister Katayama stated that gradual interest rate increases are expected as the government continues to pursue an active fiscal policy. The comments reinforced expectations that the Bank of Japan will continue moving away from its ultra-loose monetary stance, helping stabilize the yen despite ongoing dollar volatility.

Outlook for the Week Ahead

Looking ahead, markets are expected to remain driven by three major themes.

First, investors will continue monitoring developments between the United States and Iran. Any further escalation around the Strait of Hormuz could trigger another sharp rally in oil prices, increase safe-haven demand, and create renewed volatility across equity and commodity markets.

Second, attention will shift back to U.S. economic data as investors search for evidence on whether inflation is easing enough for the Federal Reserve to consider changing its policy outlook before the July FOMC meeting. Treasury yields and expectations for future interest rates are likely to remain key drivers of market sentiment.

Finally, the foreign exchange market will continue focusing on monetary policy divergence among major central banks. While the Federal Reserve maintains a cautious stance, policy moves from central banks such as the Reserve Bank of New Zealand and the Bank of Japan could create additional opportunities across major currency pairs.

Overall, investors should expect another week of elevated volatility, with geopolitics, inflation expectations, and central bank policy remaining the dominant forces shaping global financial markets.

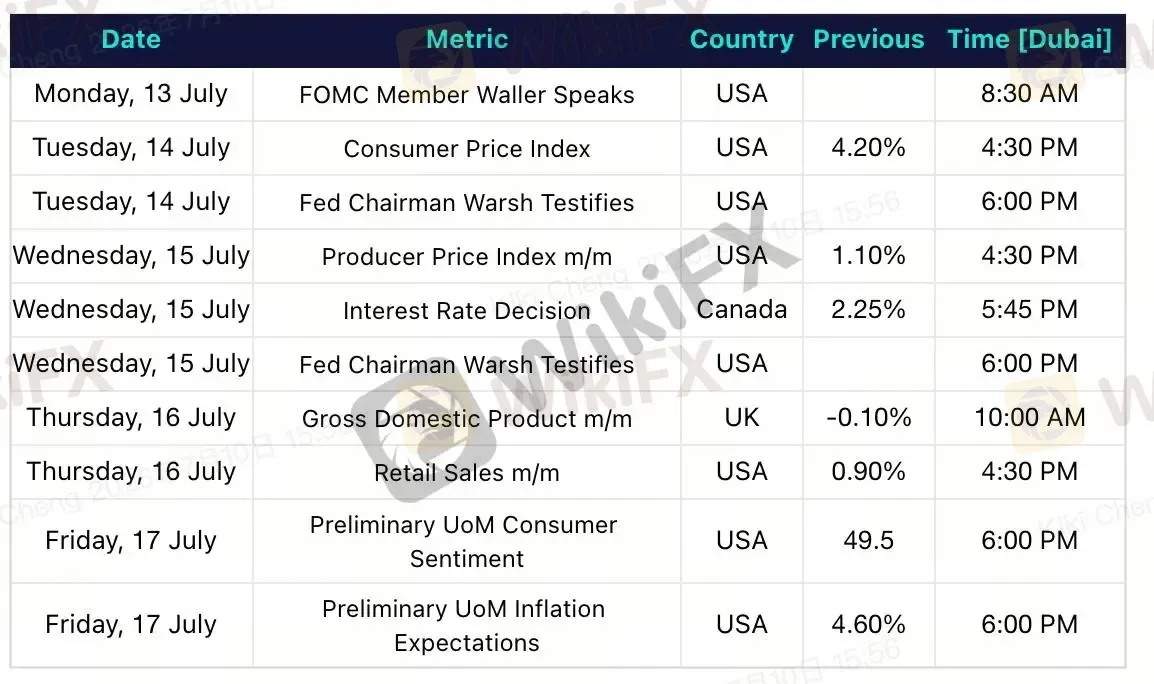

Major Economic Calendar Events for the Upcoming Week

WikiFX Broker

Latest News

WikiEXPO Hong Kong 2026 Set to Open, Bringing Together Global Fintech Leaders to Explore the Future

WikiFX

WikiFXHow the 3-Bullet Card Stops Forex Overtrading

WikiFXTRADE.COM Review 2026: Regulatory Status and Severe Withdrawal Complaints

WikiFXFunding Pips Review 2026: Is This Forex Broker Safe?

WikiFXYen Surges on Pension Plan and Strong Inflation

WikiFX⚽💱 World Cup · Forex Predict & Win Event

WikiFXCash, Luxury and Live Streams: Malaysian Police Tighten Watch on Social Media Millionaires

WikiFXFrance’s AMF Warns Against 16 Unauthorized Online Investment Entities

WikiFXCan Meta Escape a US$610 Million WhatsApp Scam Lawsuit?

WikiFXBank Customers Win Back RM211,000 After Insider Fraud

WikiFXRate Calc