Sudden Liquidation: How Deriv's "Leverage Trick" and Withdrawal Blocks Are Wiping Out Trader Account

Abstract:The WikiFX Exposure Team has analyzed a surge of urgent complaints throughout 2025 concerning the broker Deriv. While the platform boasts high influence and multiple registrations, a darker pattern has emerged in the data: a sophisticated mechanism of sudden leverage reduction and "ghost" withdrawals that leaves traders with zero balance.

The WikiFX Exposure Team has analyzed a surge of urgent complaints throughout 2025 concerning the broker Deriv. While the platform boasts high influence and multiple registrations, a darker pattern has emerged in the data: a sophisticated mechanism of sudden leverage reduction and “ghost” withdrawals that leaves traders with zero balance.

Anonymity Disclaimer: To protect the privacy of those who have stepped forward, all trader names have been omitted. The accounts and incidents described below are based on verified complaints lodged with WikiFX in 2025.

The “Leverage Switch”: A Technical Trap?

In the world of trading, leverage is a double-edged sword, but traders expect the rules to remain constant once a trade is open. However, our analysis of recent logs reveals a disturbing anomaly affecting Deriv users: the mid-trade leverage reduction.

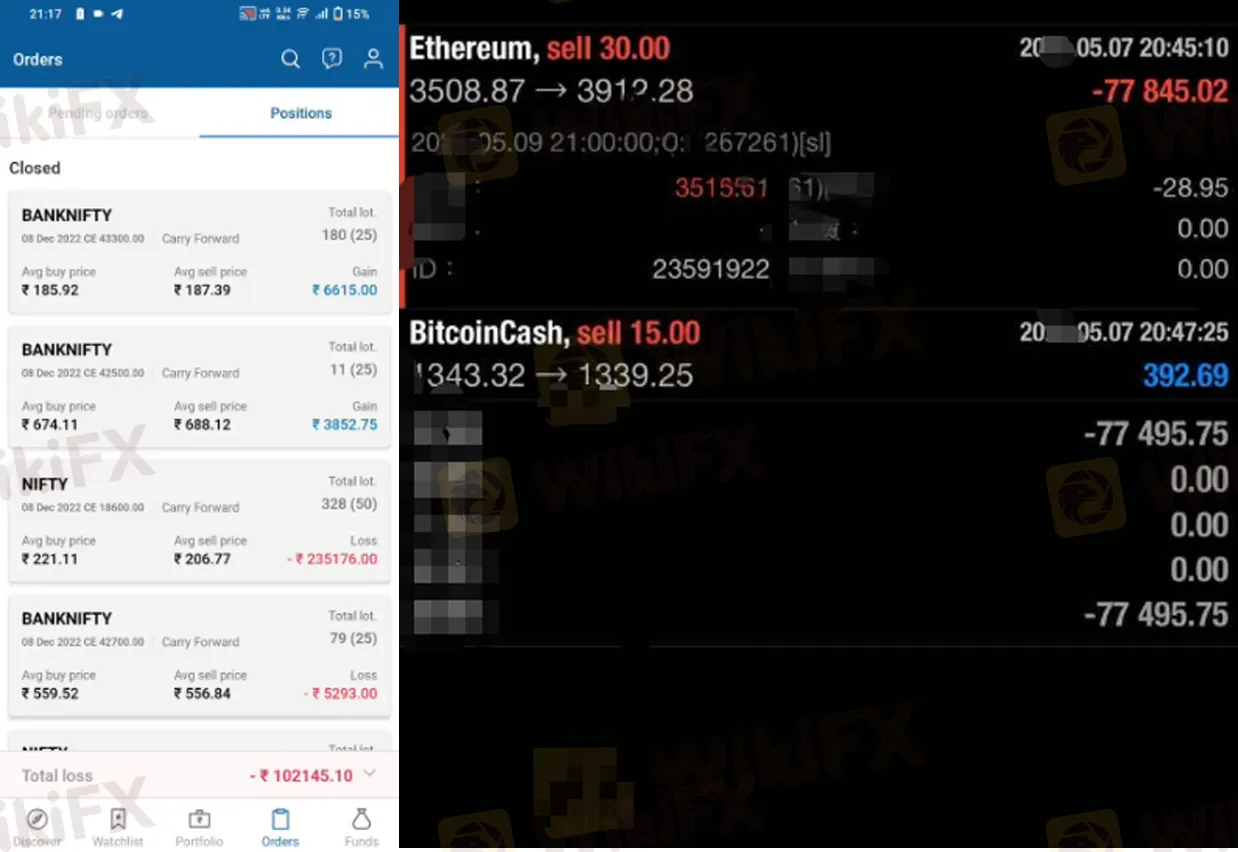

Multiple traders have reported identical scenarios occurring in late 2025. One trader, whose ordeal occurred in August, reported holding a long position on the USD/INR pair. They entered the trade based on the advertised leverage of 1:200. However, at 3:00 AM—while the market was active—the system allegedly adjusted the leverage down to 1:50 without prior warning.

The result was catastrophic. Because the account suddenly required four times the margin to hold the same position, the system triggered an immediate liquidation. The trader reported that although the market price had barely moved, the forced closure wiped out an investment of over 700,000 currency units.

Another user reported a similar incident where a 1:1000 leverage account was secretly adjusted to 1:50 during a crude oil trade, resulting in a forced loss of nearly 7,000 Australian dollars. This pattern suggests that users are not losing money to bad market calls, but to sudden changes in the platform's internal rules.

The “Ghost” Withdrawal Phenomenon

While the leverage issue destroys active trades, another issue is plaguing successful traders: the disappearance of funds during the withdrawal process.

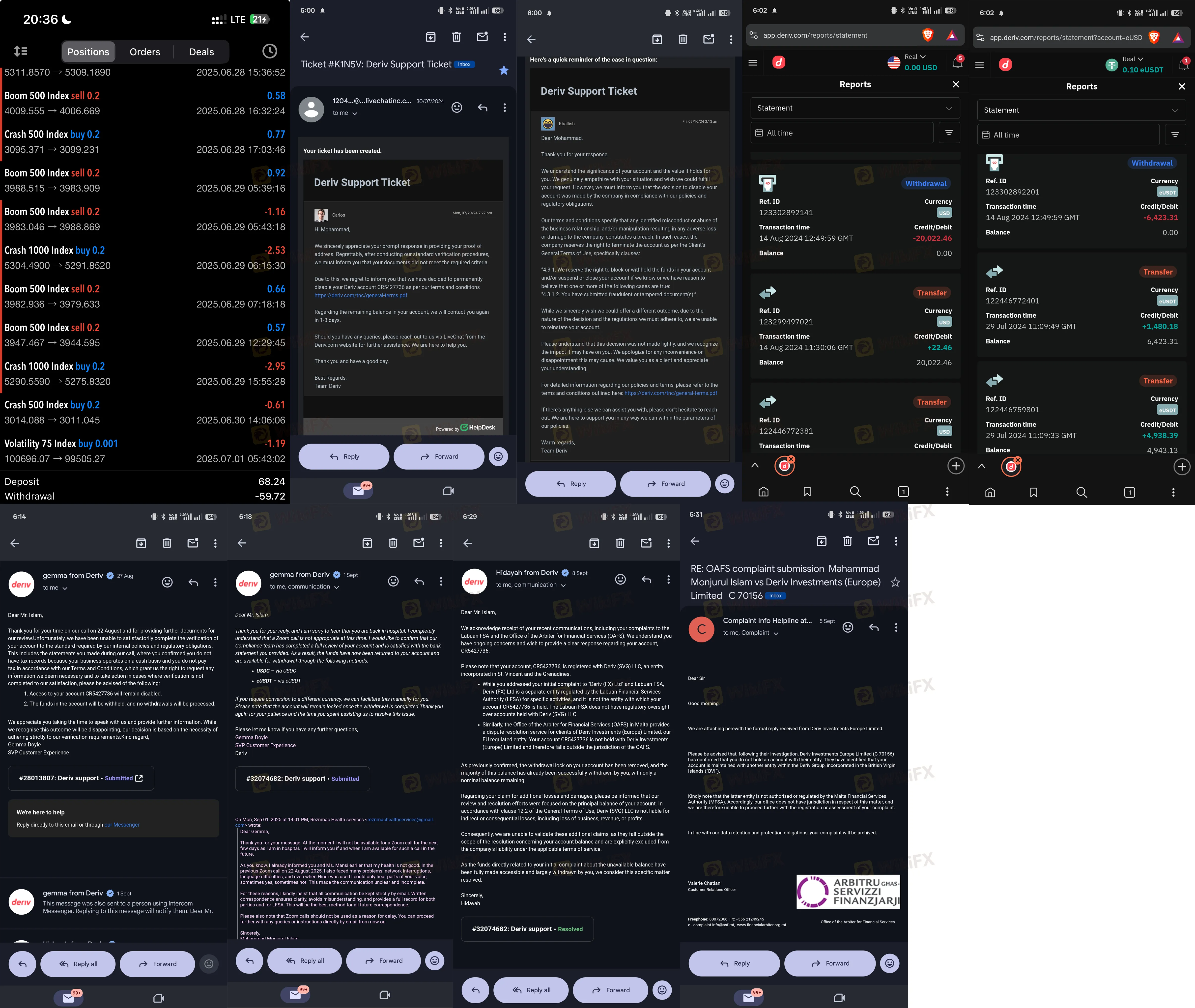

WikiFX has received numerous reports from the second half of 2025 describing a “debit without credit” error. Traders initiate a withdrawal, and the funds are immediately deducted from their Deriv trading balance. The transaction is marked as “successful” on the platform, yet the money never arrives in the user's bank account or digital wallet.

One user noted, “I made a profit and when I wanted to withdraw, they deducted money from my account but didn't credit my wallet. I complained, they said I must wait 10 business days. I still did not get my money.”

Even more alarming are reports of accounts being disabled entirely. A case recorded in September 2025 detailed how a trader's account was frozen with “false fraud allegations.” The broker allegedly unilaterally withdrew over $26,000 from the user's account without consent. It took 13 months of pressure and escalation to regulatory bodies before the user received a refund, highlighting that for some, the only way out is through external legal force.

The “KYC” Stall Tactic

When funds aren't simply missing, they are often held hostage behind a wall of bureaucratic demands. Traders have reported that after profitable periods, their accounts are frozen for “unusual trading.” To unlock the funds, Deriv support allegedly demands documentation that far exceeds standard Know Your Customer (KYC) protocols.

One trader reported being asked for six months of bank statements, proof of funds, and tax returns. Even after submitting these documents, the user was asked to pay a 10% “verification fee”—a classic red flag in the industry. Legitimate brokers deduct fees from the balance; they rarely ask for external payments to release existing funds.

Regulatory Audit: The Disconnect

Deriv presents itself as a highly regulated entity. However, a deep dive into the regulatory database shows a complex picture. While they hold several licenses, there are critical gaps and warnings that African traders must be aware of.

Deriv Regulatory Status Table

| Regulator Name | Country/Region | License Type/Status |

|---|---|---|

| Cayman Islands Monetary Authority (CIMA) | Cayman Islands | Exceeded (High Risk) |

| British Virgin Islands FSC | British Virgin Islands | Offshore Regulation |

| Vanuatu Financial Services Commission (VFSC) | Vanuatu | Offshore Regulation |

| Malta Financial Services Authority (MFSA) | Malta | Regulation in Progress |

| Labuan Financial Services Authority (LFSA) | Malaysia | Regulation in Progress |

| Securities and Commodities Authority (SCA) | UAE | Regulation in Progress |

Note: The status “Exceeded” for the Cayman Islands license indicates the broker may be operating outside the permitted scope of that specific license. Furthermore, regulatory disclosures show that Indonesian authorities (Bappebti) have previously blocked hundreds of domains associated with this entity for operating without local authorization.

A Pattern of “Price Jumps”

Beyond withdrawals and leverage, technical anomalies in price feeds have triggered accusations of manipulation. Analysis of trader logs from August 2025 shows complaints regarding “price jumps” in the final seconds of binary or options contracts.

One detailed report claimed that when prices approached critical profit levels, quotes would jump 0.2 to 0.5 pips in the opposite direction within the last five seconds. The user alleged this occurred in 77% of their tracked cases, turning wins into losses. While market volatility exists, consistent adverse movement in the final seconds of a contract raises serious questions about execution fairness.

Conclusion and Warning

The disparity between Deriv's “AAA” influence ranking and the experience of individual traders is stark. The data indicates that while the platform is massive and holds various offshore registrations, specific mechanisms—sudden leverage reduction, withdrawal freezes, and excessive documentation demands—are causing significant financial harm to traders.

WikiFX advises all investors to exercise extreme caution. The presence of valid offshore licenses does not automatically protect you from the operational irregularities described above.

Forex and CFD trading involves a high level of risk and may not be suitable for all investors. The data provided in this article is based on actual complaints and regulatory records lodged with WikiFX in 2025. Please prioritize the safety of your principal over potential profits.

Read more

Exposure: NAGA’s "Phantom Bonus" Trap and the $80,000 Silent Treatment

While NAGA markets itself as a comprehensive "communal trading ecosystem" backed by European regulation, recent distressing reports from mid-2025 suggest a darker reality for profitable traders. With allegations of high-value accounts being wiped under the guise of "expired bonuses" and senior executives blocking distressed clients, we investigate whether this FinTech giant is currently safe for your capital.

4XC Exposed:Do Traders Report Sudden Balance Disappearance, Outdated Process & Poor Customer Service

Have you experienced a NIL balance in your 4XC trading account due to a sudden liquidation of your forex positions? Gained a healthy return on your deposit but saw a quick disappearance of funds in your account afterward? Do you still need to go through the old and outdated process of opening a 4XC Broker trading account? Are you struggling to withdraw your funds? These have allegedly become rampant for traders tied to this broker. In this 4XC review article, we have shed light on the negative comments. Take a look!

TOPONE Markets Review: Allegations of Withdrawal Denials, Forced Liquidations & Questionable Rules

Do you think that TOPONE Markets’ forex trading rules need to change? Do these rules prevent you from earning profits? Does the forex broker adopt a dubious approach by ensuring fast deposits but delayed withdrawals? Have you witnessed forced liquidations of forex positions by the Cayman Islands-based broker? In this TOPONE Markets review guide, we have shared several complaints against the broker. Read on!

The "Royal" Treatment? How "AI" Promises and Withdrawal Taxes Are Trapping Traders

Traders flock to OneRoyal drawn by the allure of "AI-driven" returns and a prestigious name backed by global licenses. However, a disturbing pattern has emerged from the chaotic data streams: accounts are being drained not just by market forces, but by "artificial" spread widening, erratic price data that defies global benchmarks, and—most alarmingly—arbitrary demands for "tax clearance certificates" to release funds.

WikiFX Broker

Latest News

Is Deriv Safe? A Deep Dive into Regulatory Claims vs. Withdrawal Nightmares

WikiFX

WikiFXInside Darwinex Broker Review: Regulation Explained & Authentic User Complaints

WikiFXMIFX Regulation, Is This Indonesian Broker Safe?

WikiFXBLITZ finance Review 2025: Is It a Scam? License and Safety Evaluation

WikiFXThe "Invalid Profit" Trap & The Withdrawal Maze: A Deep Dive into MultiBank Group

WikiFXB2CORE Update Enhances Forex Broker Operations and CRM Systems

WikiFXWisunoFX Review 2025: A Complete Look at Costs, Trading Platforms, and Safety

WikiFX9X Markets Review: Is It Reliable?

WikiFXIQ Option Review: Real User Experiences

WikiFXBessent to propose major overhaul of regulatory body created from financial crisis

WikiFXRate Calc